Building credit in Canada requires time, responsible borrowing and consistent payments. Whether you are a newcomer, student or young adult with no credit history, the basic strategy is the same: start with one manageable credit account, pay every bill on time and avoid using too much of your available credit.

Your Canadian credit score is a three-digit number based on information in your credit report. Scores usually range from 300 to 900, and lenders may use them when deciding whether to approve applications and what interest rate to offer. Your score can change as lenders report new account activity. (Canada)

This guide explains how to build credit in Canada, what mistakes to avoid and how newcomers and students can start building a reliable credit history. This article provides a practical explanation of how to build credit in Canada without carrying unnecessary debt or paying avoidable interest.

Important: No company or strategy can guarantee a specific credit score or a fixed improvement timeline. Your results depend on your entire credit file, the information lenders report and the scoring model being used.

What Does It Mean to Build Credit in Canada and Why Does It Matter?

Building credit means creating a record that shows lenders how you manage borrowed money.

A Canadian credit report may include information about:

Credit cards

Personal loans

Lines of credit

Car loans

Mortgages

Payment history

Credit limits and balances

Credit applications

Accounts sent to collections

Canada’s two main credit bureaus are Equifax and TransUnion. They collect information about credit activity in Canada and use that information to create credit reports and scores. (Canada)

If you recently arrived in Canada, begin by reading WiseBlog’s guide to opening your first bank account in Canada.

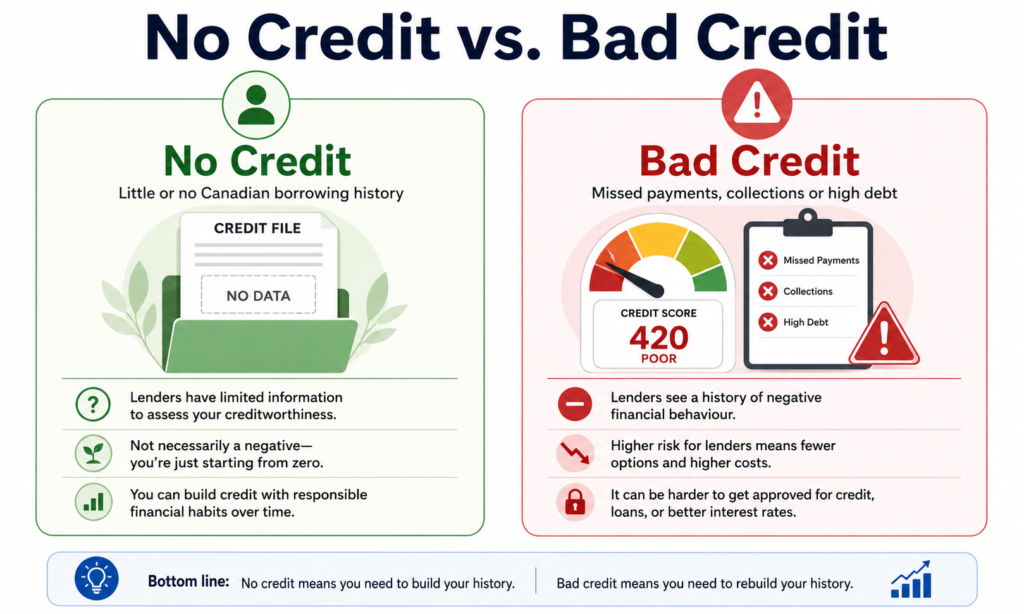

No Credit vs. Bad Credit

Before learning how to build credit in Canada, it is important to understand whether you have no credit history or a damaged credit history.

Understanding the difference between no credit and bad credit is important when learning how to build credit in Canada the right way.

| Situation | What it means | Main challenge |

|---|---|---|

| No credit | You have little or no borrowing history in Canada | Lenders have limited information about you |

| Thin credit file | You have only one or two recent accounts | Your history may be too limited for some lenders |

| Bad credit | Your report contains missed payments, high balances, collections or other negative activity | Lenders may consider you a higher-risk borrower |

A newcomer or student may have no Canadian credit history without having made any financial mistakes. The goal is to start carefully and build a positive record over time.

1. Open a Canadian Bank Account

A chequing or savings account does not normally build your credit score by itself. However, it makes it easier to manage credit responsibly.

A Canadian bank account can help you:

Receive employment or benefit payments

Pay bills electronically

Set up automatic credit-card payments

Avoid missed payment dates

Build a relationship with a financial institution

Compare monthly fees, transaction limits, minimum-balance requirements and newcomer or student offers before selecting an account.

For broader guidance on saving, budgeting and managing expenses, read WiseBlog’s Personal Finance Canada guide.

2. Apply for a Suitable First Credit Card

For many beginners, learning how to build credit in Canada starts with choosing one suitable credit card and managing it responsibly.

A credit card can help establish Canadian credit when the issuer reports your account activity to Equifax or TransUnion.

Possible first-card options include:

A newcomer credit card

A student credit card

A low-limit unsecured card

A secured credit card

Do not choose a credit card only because it offers points or a welcome bonus. Compare:

Annual fee

Interest rate

Eligibility requirements

Credit limit

Foreign-transaction fee

Grace period

Whether the issuer reports to Canadian credit bureaus

Use the card for one or two normal expenses, such as groceries, a phone bill or transportation. Do not treat your credit limit as additional income.

3. Consider a Secured Credit Card When Necessary

A secured credit card usually requires a refundable security deposit. That deposit reduces the issuer’s risk and may determine the card’s credit limit.

A secured card may be useful when:

You have no Canadian credit history

You were declined for an unsecured card

You are rebuilding after previous payment problems

You have a limited or thin credit file

Before applying, confirm:

The required deposit

Annual and monthly fees

Interest rate

Refund conditions

Whether account activity is reported to both credit bureaus

A secured credit card should be used like a regular credit card. Keep the balance manageable and pay on time.

A prepaid card is different. A prepaid card generally uses money that you load in advance and may not build credit.

4. Pay Every Bill on Time

The most important rule for how to build credit in Canada is to make every required payment by the due date.

Payment history is one of the most important components of a credit profile. The Financial Consumer Agency of Canada recommends always paying bills on time and making at least the minimum payment when the full amount cannot be paid. (Canada)

Use these safeguards:

Turn on payment reminders

Set up automatic payments

Review statements before the due date

Pay at least the minimum amount by the deadline

Pay the full statement balance whenever possible

Keep enough money in your bank account for automatic payments

Paying only the minimum can keep an account current, but it usually increases the time and interest required to repay the balance. (Canada)

You do not need to carry a balance or pay interest to build credit. The Government of Canada recommends aiming to pay the credit-card balance in full by the due date each month. (Canada)

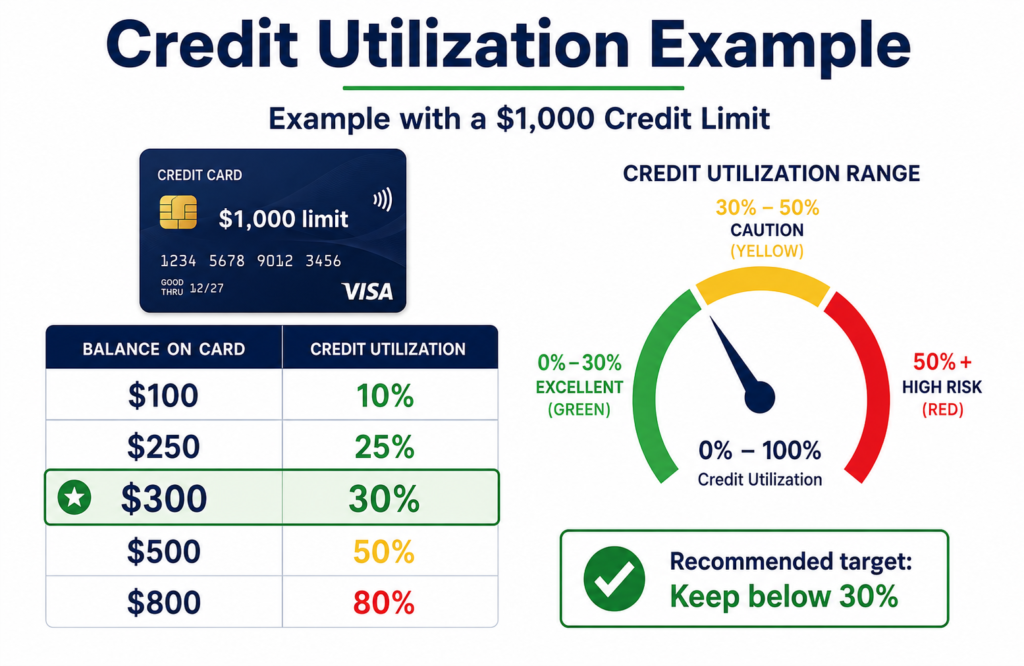

5. Keep Credit Utilization Below 30%

Understanding credit utilization is a major part of how to build credit in Canada, because using too much available credit may concern lenders.

A major part of how to build credit in Canada is using only a small portion of your available credit limit.

Credit utilization is the percentage of your available revolving credit that you are using.

The Financial Consumer Agency of Canada recommends trying to use less than 30% of your total available credit. It also notes that high utilization can concern lenders even when the balance is paid in full each month. (Canada)

Example with a $1,000 credit limit

| Balance | Utilization |

|---|---|

| $100 | 10% |

| $250 | 25% |

| $300 | 30% |

| $500 | 50% |

| $800 | 80% |

With a $1,000 limit, try to keep your reported balance below $300.

With a $1,000 limit, try to keep your reported balance below $300.

This does not mean that you should deliberately spend $300 every month. Spend only what fits your budget.

A practical approach is to make an extra payment before the statement is issued when your balance becomes unusually high.

6. Limit New Credit Applications

Applying selectively is another important part of how to build credit in Canada, especially when your credit file is still new.

When you apply for a credit card, loan or certain other products, the lender may perform a hard credit inquiry.

Too many hard inquiries in a short period can make lenders think that you urgently need credit or may be borrowing beyond your means. (Canada)

Use this approach:

Review eligibility requirements before applying.

Select one suitable product.

Submit one application.

Use the account responsibly for several months.

Avoid applying repeatedly after a decline.

Checking your own credit report is considered a soft inquiry and does not affect your score. (Canada)

7. Keep Older Accounts Open When Appropriate

The age of your credit accounts can affect your overall credit history. Keeping an older account open may help maintain a longer record and preserve your available credit. (Canada)

Do not automatically close your first credit card after receiving a newer card.

Keeping an older account may make sense when:

It has no annual fee

You can monitor it safely

You are not tempted to overspend

It helps preserve available credit

There is no security concern

Closing it may make sense when:

It has an expensive annual fee

It creates overspending risk

The account is no longer secure

You cannot manage multiple accounts responsibly

Canada’s consumer guidance also notes that keeping one manageable, low-limit account open may help maintain or improve credit history. (Canada)

8. Check Your Equifax and TransUnion Credit Reports

You can access your credit report online for free from both Equifax and TransUnion. The two reports may not contain exactly the same information, so review both. (Canada)

Look for:

Accounts you do not recognize

Incorrect names or addresses

Payments incorrectly marked late

Wrong credit limits

Outdated balances

Duplicate accounts

Closed accounts shown as open

Signs of identity fraud

You should consider checking your reports before applying for an important credit product, renting an apartment or financing a vehicle.

Use the Government of Canada’s official instructions for getting your credit report and credit score.

9. Dispute Incorrect Information

Incorrect information can negatively affect your credit profile.

You have the right to dispute information that you believe is wrong, and credit bureaus must correct verified errors without charging you. (Canada)

Follow these steps:

Gather statements, receipts and other supporting documents.

Contact the lender that reported the information.

Submit a dispute to Equifax or TransUnion.

Keep copies of every form and message.

Review your report again after the investigation.

Accurate negative information generally cannot be removed simply because you dislike it. Disputes are meant for information that is inaccurate, incomplete or fraudulent.

How Newcomers Can Build Credit in Canada

The basic principles of how to build credit in Canada apply to everyone, but newcomers may face additional challenges because foreign credit history usually does not transfer automatically.

Newcomers may arrive with savings, income and responsible borrowing experience from another country but still have no Canadian credit file.

Canadian credit bureaus collect information about credit activity in Canada, so foreign credit history does not automatically become part of your Canadian report. (Canada)

A simple newcomer strategy is:

Open a Canadian bank account.

Ask about newcomer credit-card programs.

Compare the fees and requirements.

Apply for one suitable card.

Add one small recurring bill.

Set up automatic payment.

Keep utilization below 30%.

Review both credit reports after several months.

Some financial institutions may review foreign banking records, employment information or international relationships. Their policies differ, so ask before applying.

For more help, read WiseBlog’s guide to opening your first bank account as a newcomer.

Students researching how to build credit in Canada should prioritize low fees, small purchases and automatic payments.

How Students Can Build Credit in Canada

Students should focus on manageable borrowing rather than obtaining the highest possible credit limit.

A simple student strategy is:

Select a no-fee or low-fee student card

Use it for one predictable monthly expense

Keep utilization low

Pay the full statement balance

Avoid cash advances

Avoid repeated applications

Review spending weekly

Follow a monthly budget

Before taking on a new payment, estimate whether it fits your budget. You can also use OmniTools.ca for practical online calculators and everyday tools.

Your First 30 Days: Credit-Building Checklist

The following checklist turns the advice on how to build credit in Canada into a manageable first-month plan.

Week 1: Prepare

Open or review your Canadian bank account.

Create a simple monthly budget.

Gather identification and proof of address.

Gather proof of income or student status when required.

Compare suitable beginner credit cards.

Week 2: Apply carefully

Select one appropriate card.

Read the fee schedule.

Review the interest rate and grace period.

Submit only one application.

Avoid applying for several products at once.

Week 3: Set up the account

Activate the card securely.

Create account alerts.

Add one small recurring expense.

Set up automatic payment.

Store your account details safely.

Week 4: Build the routine

Review your card balance.

Keep utilization below 30%.

Pay by the due date.

Check for unauthorized transactions.

Record the payment in your budget.

Six-Month Credit-Building Plan

| Month | Main action | Objective |

|---|---|---|

| Month 1 | Open one suitable credit account | Begin your Canadian credit history |

| Month 2 | Use the card for one planned expense | Create manageable account activity |

| Month 3 | Continue paying on time | Establish payment consistency |

| Month 4 | Review spending and utilization | Keep borrowing under control |

| Month 5 | Check both credit reports | Identify possible errors |

| Month 6 | Review your progress | Continue without unnecessary applications |

Six months is not a guaranteed timeline for obtaining a particular score. Strong credit is built through repeated responsible behaviour over a longer period.

Common Credit-Building Mistakes

Carrying a balance to build credit

You do not need to pay interest to build credit. Use the account and pay the statement balance by the due date.

Using most of the credit limit

High utilization may make you appear dependent on borrowed money.

Applying for several cards at once

Multiple hard inquiries can affect your score and increase the risk of overspending.

Paying after the due date

A payment made after the deadline may still be considered late, even when you pay the entire balance.

Ignoring small bills

Unpaid phone, internet, utility or credit accounts may eventually be reported or sent to collections.

Closing your first account too quickly

Closing an older account can reduce available credit and shorten your active history.

Co-signing without understanding the responsibility

A co-signer can become responsible for the debt. Missed payments may affect both people.

Paying a company that guarantees a score increase

Be cautious of businesses promising to remove accurate information or guarantee a specific score by a particular date.

Many people searching for how to build credit in Canada want to know how long it takes, what mistakes to avoid, and whether newcomers can start from zero.

Frequently Asked Questions

How long does it take to build credit in Canada?

There is no fixed timeline. Your file may begin after a lender reports an account, but developing a strong history requires consistent payments and responsible borrowing over time.

What is a good credit score in Canada?

Canadian credit scores usually range from 300 to 900, with higher scores generally considered better. Individual lenders set their own approval standards. (Canada)

Can I build credit without a credit card?

Yes. Certain reported loans and other credit products may contribute to your history. However, a manageable credit card is one of the most common starting options.

Should I carry a balance to build credit?

No. Carrying an unpaid balance does not provide a special credit-building benefit and may result in interest charges.

Does checking my own credit lower my score?

No. Requesting your own report is a soft inquiry and does not affect your credit score. (Canada)

What credit utilization should I aim for?

Try to use less than 30% of your total available credit. Lower utilization may be preferable when it occurs naturally within your budget. (Canada)

Can newcomers transfer their foreign credit score to Canada?

Foreign credit scores generally do not transfer directly into Canadian credit-bureau files. A lender may independently consider foreign records, but its policy will vary.

Can international students build credit in Canada?

Yes. Eligible international students may be able to apply for student, newcomer or secured credit cards. Approval requirements differ between financial institutions.

Is a secured credit card the same as a prepaid card?

No. A secured credit card is a credit account supported by a security deposit. A prepaid card normally uses funds loaded in advance.

Can paying rent build credit in Canada?

Rent may affect credit only when the payment information is reported through an eligible service or arrangement. Confirm the fees, reporting method and participating credit bureau before enrolling.

Learning how to build credit in Canada is not about finding shortcuts. It is about building strong habits over time. If you want to know how to build credit in Canada successfully, focus on paying on time, keeping balances low, avoiding unnecessary applications, and checking your credit reports regularly. With patience and consistency, newcomers, students, and beginners can build a healthy Canadian credit profile.

Final Thoughts

Learning how to build credit in Canada is not about finding a shortcut. It is about establishing reliable financial habits.

Start with one suitable account, pay every bill on time, use less than 30% of your available credit, avoid unnecessary applications and review both credit reports for errors.

For more Canadian money guidance, explore:

Personal Finance Canada: Complete Guide to Budgeting, Saving and Building Wealth

Opening Your First Bank Account in Canada: A Guide for Newcomers

Disclaimer

This article provides general educational information and does not constitute personalized financial, credit, legal or tax advice. Credit-card terms, lender requirements and reporting practices may change. Review the official terms of any product before applying.